Reasons to Lease

Reasons to lease

1. Ability to have a new car every two or three years

With all of the new safety, style and efficiency improvements that have and will happen, Leasing allows you to stay current and up to date and also allows you to plan as the costs are predetermined and fixed.

2. Gap Protection

In the event of a total loss, the whole balance of the lease/residual is paid off, regardless of the actual market value of the vehicle, which is all that your casualty insurance will pay.

3. Limited Liability

The owner of the vehicle has primary liability. In the case of a lease, the vehicle owner is the company that leases you the vehicle, not the driver. The leasing company carries an umbrella policy, which covers everything over your primary liability limit.

5. Help in borrowing

The entire debt does not show on a balance sheet; therefore, a leased car does not show up as a liability on a loan application.

6. Tax Ramifications Have Changed to the Benefit of a Business Owner

The bigger the lease payment, the bigger the deduction, provided that the vehicle is used more than 51% of the time for business.

7. No depreciation risk

The guaranteed future value of the vehicle is the amount deducted at the beginning of the lease. It is also the expected value of the vehicle at the end of the lease. You have the term of the lease to decide if you want to complete the purchase.

- If the guaranteed future value compared to the actual market value at the end of the lease favors you, you complete the purchase.

- If it doesn't favor you, you simply turn the vehicle back to the lessor.

8. Sales Tax Savings

The only thing better than a tax deduction is never having to pay the tax in the first place. The tax advantage of leasing is that you only pay tax on the monthly payments. i.e. You would pay 8-10% of 100% in a buy situation, OR you can pay only the tax on 50% in a lease, based on the guaranteed future value.

Common Objections to Leasing

1. "I won't own it. I have no equity."

That's good, not bad! You won't have any equity because you won't pay for any equity. That's why your payment is so low. In order to have equity in the vehicle, or own the vehicle, your payment would have been much higher. Instead of equity in the vehicle, you have cash. You can use this cash to buy the vehicle if you want, but you don't have to decide until the end of the lease. Some assets are good to own, like a house or stocks, because they have the possibility of appreciating.

Vehicles do not appreciate; they depreciate. Would you pay $100,000 for a house if you thought it would be worth $75,000 in three years?

2. "I've had a bad experience with leasing or someone I know had a bad experience."

It's true. Some people have gotten burned in leasing. It's because they were put into the wrong lease or it wasn't fully explained to them. Many people were put into an open-end lease and didn't realize they were guaranteeing the residual at the end. We don't offer open-end leases. We offer closed end leases. In other cases, perhaps they exceeded the 15,000-mile per year allowance or had a charge back for abnormal wear and tear. If they had purchased the same vehicle and drove the same number of miles, or traded it in the same condition, they would have experienced the same deductions.

We won't let that happen to you. We tailor the lease specifically to your needs and let you know what your rights and obligations are up front.

3. "I drive too many miles" or "I don't drive enough miles."

If you drive more than 15,000 miles per year you are an ideal leasing candidate. You can build the extra miles into the lease at .10 per mile or pay .15 per mile at the end of the lease. Which would you prefer?

.10 per mile is quite a savings for you. If you buy the same vehicle and drive the same number of miles, when you go to trade it in, they will deduct .25 to .30 per mile, over 15,000 miles, to get the appraised value. You can actually buy the miles you need cheaper in a lease than you can from yourself!

4. "I don't understand leasing."

Don't feel bad, very few people do. Worse yet, some think it is renting. Leasing is probably the most misunderstood consumer transaction in America.

Unfortunately, what has kept many people from leasing is the fear of the unknown.

According to a survey by J.D. Powers and Associates, once people have leasing explained and they try it, 93% of them are so satisfied they lease their next vehicle! We don't view leasing as just another way to buy a car. We view it more as an insurance policy. It removes the risk of the vehicle's depreciation. Leasing offers value; ownership does not.

Leasing gives you the ability to pay for the part of the vehicle you use, and give you a choice of "purchasing" after you have driven it for a few years.

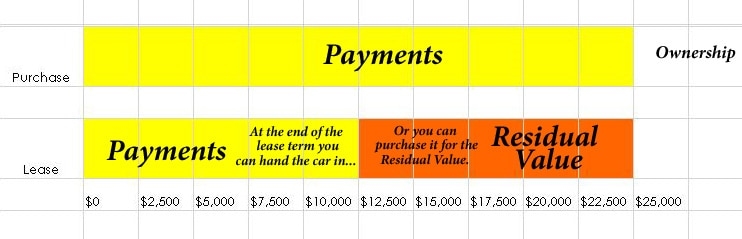

This graph demonstrates how a lease differs from a traditional purchase. Two identical vehicles each with a cost of $25,000 are shown. One is purchased and after paying $25,000, you own the car. With the lease you make payments for the lease term (usually 36 months), and then have a choice. You can hand the car back in to Palm Springs Subaru, you can purchase the vehicle for the residual value or you can trade it in and use the equity, if any, towards another Subaru. The residual value is the predetermined value of the car after the lease term. One thing to keep in mind is vehicles that hold their value generally are better vehicles to lease. If the residual value is higher at the end of the lease, your payments will be lower during the lease term. The graph below demonstrates a residual of 50%.